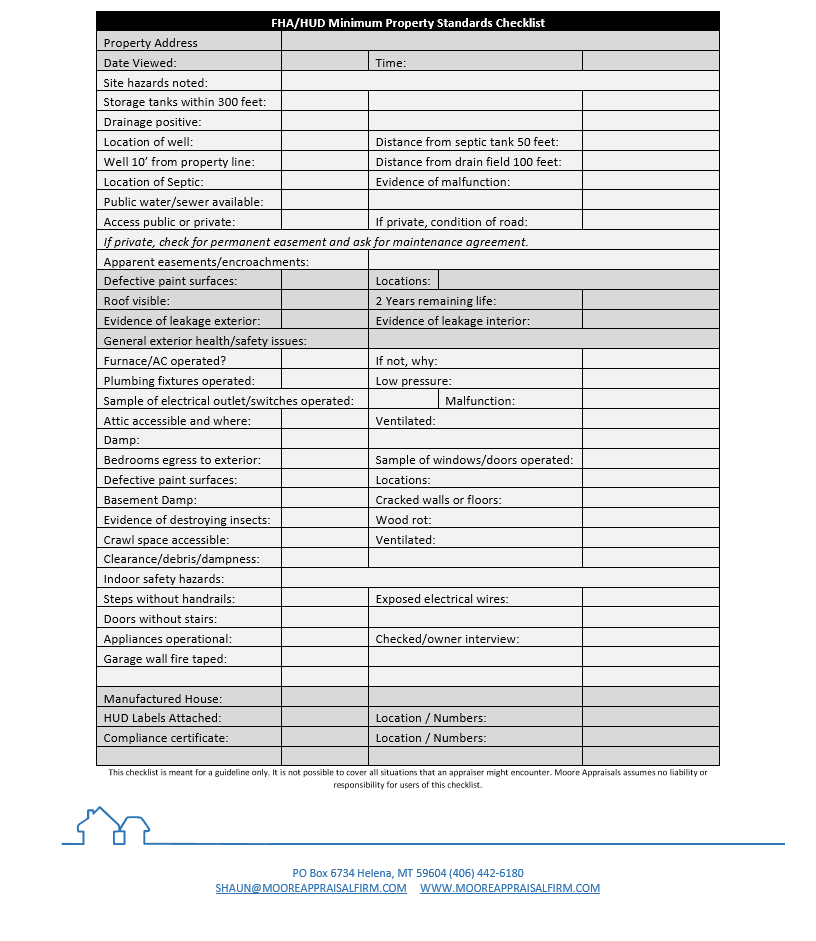

Based on the client’s intended use of the appraisal, the appraiser determines whether an interior and/ or exterior inspection or no inspection required. Under many circumstances, the lender will require a full viewing of the property including an exterior and interior inspection. Assuming that a complete inspection is required, the appraiser inspects the site, site improvements, and building improvements. The appraiser consider the site’s size, shape, topography, drainage, and any other attributes that may affect value. He or she views the site improvements (e.g. , paving, fences, and walls, landscaping) to determine their contribution of value to the property. Finally, the appraiser inspects any structures. Some of the items considered are building style, number or stories, size, number or rooms (including bedrooms and baths, etc). He or she observes the structure’s condition as an aid to estimation depreciation. In addition, the appraiser considers the property as a whole, including the dwelling and any other improvements as well as any visible encumbrances (e.g. power lines, encroachments). Finally, the appraiser considers the property in relation to the neighborhood.An appraiser’s inspection and a home inspection are different. An appraiser gathers information to develop a value opinion and a home inspector gathers information to identify construction features, structural integrity, and any needed repairs.